Video on Long Term Care

To Watch a Short Video About Long Term Care Click Here

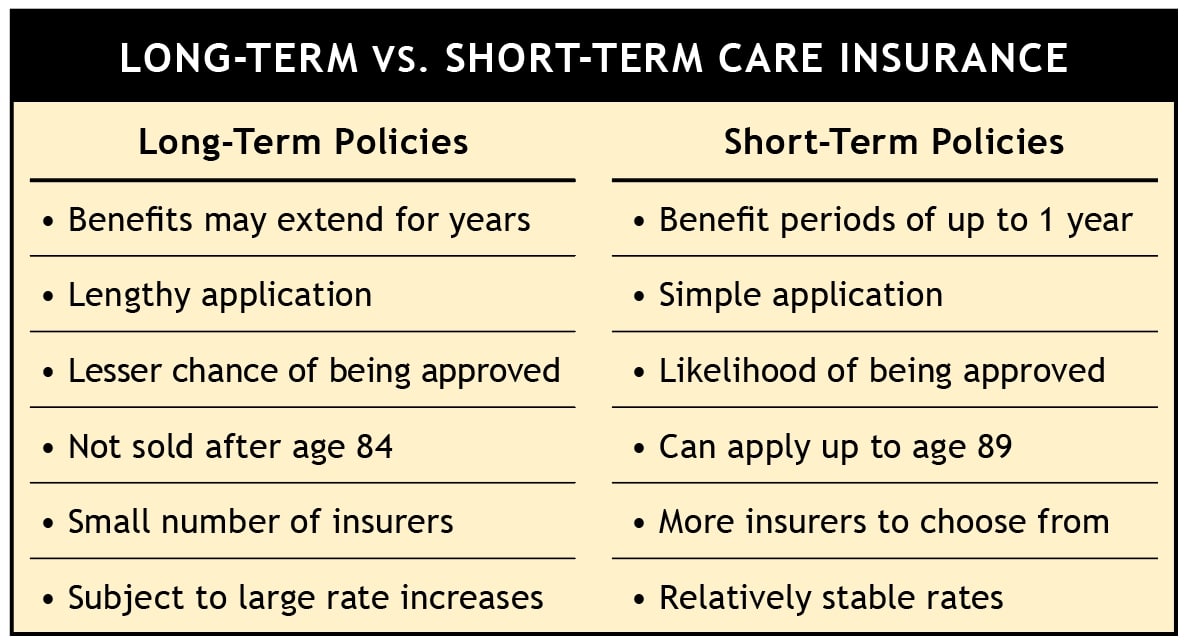

What is Long Term Care Insurance?

Long Term Care is services that helps meet the medical and non-medical needs of people with chronic illness or disabilities who cannot care for themselves for long periods of time. These services include dressing, bathing, transferring (to or from bed to chair), incontinence, eating and using the bathroom. These services can be provided at home, in the community, in assisted living facilities or in nursing homes.

Long term care insurance was developed to provide the needed financial protection against the cost of long- term care that regular health insurance and Medicare do not cover. Long-term services can last years and can be very expensive. These insurance policies can be purchased based on the need for care. Some plans pay a daily benefit for a duration of time like 2 or 3 years and some pay until a maximum dollar amount has been paid. You can build the policy with an inflation rider to use the premiums as a tax deduction and to keep up with the rising cost of health care.

Who should get this coverage and why do I need it?

- It is never too early to consider long term care insurance, the younger you are the less expensive it will be. Anyone age 45 or older, NOW is the time to start planning.

- The coverage is guaranteed renewable for life if you make the payments

- You have to health qualify for these products, so if you wait until something has happened and you need the services, it will be too late.

- 70% of all people age 65 and up will use long term care at some point in their lives. That is 7 out of 10 people. That is a very high number to consider.

- This coverage will protect your retirement assets that you worked your whole life to achieve.

- This will reduce the emotional and financial stress on you and your family with care giving responsibilities.

- You can make the decision to stay in your home for care, or chose the assisted living or nursing home facility of your choice.

Myths surrounding Long Term Care

1. I am probably already covered for long term care.

ANSWER: Most people think their insurance covers long term care expenses, but that is not true. Long term care is NOT covered on other insurances. Long term care insurance policies cover day to day personal care assistance, when you are not able to perform everyday tasks like bathing and dressing

2. Medicare or Medicaid will cover my long-term care.

ANSWER:Medicare does not cover long term care. Medicare pays for skilled care in a nursing home, only for short periods of time (up to 100 days), while recuperating following a hospital stay. Medicare does not cover personal or custodial care costs. Medicaid does pay for long term care, but only after you spend down all of your assets and income.

3. Long term care is only for the elderly.

ANSWER: Long term care is not just for the elderly, younger people may need it due to unexpected illnesses, diseases, injuries, or accidents.

4. I won’t need long term care insurance because my family will be able to care for me.

ANSWER: Families do and will help provide care for you, but when it is time for professional help or staying in a nursing home, they generally cannot afford to pay those costs for you.

5. I can’t afford long term care insurance.

ANSWER: Long term care insurance can be more affordable than you thought and can be tailored to meet your needs and budget. The costs can be managed by making a retirement plan that is right for you. The younger you are when you purchase this insurance, the lower the premiums.

How much Long-Term Care Insurance do I need?

The cost of these policies vary by state and by region. Where you retire helps determine the amount of coverage you will need. The type and duration of care, the provider you use and where you live are huge factors.

In 2021, the national average costs for long term care in the US was:

- $7756 a month for semi private rooms in a nursing home

- $8821 a month for private rooms in a nursing home

- $4300 a month for assisted living facility

- $74 a day for services in an adult day care center

In 2020, Missouri had the cheapest semi private room at $5080 and private room at $5749 per month, but Alaska had the most expensive with semi private rooms for $37,143 and private rooms for $36,378 per month. So, you can see geography makes a difference.

It is projected for the national average costs for long term care in the US to be:

2030 cost of semi-private room will be $10,423 and private room will be $11,855

2040 cost of semi-private room will be $14,008 and private room will be $15,932

Example: In Missouri for a private room, it is $5749 a month in 2020 x 12 months = $68,988 per year, (Factor in 3.5% medical inflation rate) $97,314 per year in 10 years or $132,630 per year in 20 years

Average length of time for men is 2.2 years x $132,630 = $291,786

Average length of time for women is 3.7 years x $132,630 = $490,731

Alzheimer’s patients average is 8 years x $132, 630 = $1,061,040

These numbers may be confusing to you, please reach out to us and we can explain exactly how we came up with those figures. If you want to do a calculation for another state, we can do that also. Imagine how much more the Alaska numbers would go up with the pricing being so much higher there.

Different types of care

Long Term Caretakes place in a nursing home that provides custodial care, but may include skilled care, intermediate care, and custodial care. The patient can be transferred within the facility as their needs change. Nursing homes provide a great range of 24-hour care.

Home Health Care is used for recovering from an injury or illness and 24-hour care is not needed. This is most often custodial care provided by visiting nurses, therapists, or home health aides. Services may include things like respiratory therapy, cleaning and bandaging of wounds, monitoring health and assistance with bathing and dressing.

Adult Day Care centers provide care in a group setting for aged or disabled people who live at home, and/or may need help with the basic activities of daily living due to physical or mental impairment. These centers usually provide elderly people with social interaction, therapeutic activities, preventive health services, and nutritional meals.

Hospice Care is compassionate care for those terminally ill patients nearing the end of life. This care tries to make the patient as comfortable as possible until the end, it can take place in a facility or at home.

Respite Care provides some time off for the caregiver (usually a relative) who regularly provides care for an elderly or disabled person. This can be offered in a community center, nursing home, or at home through a service.

Traditional Long Term Care vs Hybrid Long Term Care

With traditional long term care insurance, you pay the premiums, and when you need it due to age or illness, the policy pays out a daily benefit. Some people feel they are “throwing away “money if they die and never use the insurance.

- These plans have huge flexibility for monthly benefits, benefit period, inflation protection and waiting period.

- Traditional long-term policies can have the option of being tax qualified.

- They are guaranteed renewable if you pay the premium.

- Premiums are paid monthly, quarterly, semi-annual, or annually.

Hybrid long term care plans allow you to draw funds from the policy for your long-term care, and the insurance company pays for the care when the funds run out. With these plans, if you die without using the coverage, your beneficiary receives the money as a death benefit (like life insurance).

- If you pay your premiums, you will have a contractually guaranteed death benefit, guaranteed cash value and guaranteed amount of long-term care coverage.

- These plans allow you to choose your options at the beginning but very little flexibility afterwards.

- Some of these plans can be purchased as a one-time lump sum and others can be paid over a short period of time, which can make them very costly.

- Hybrid policies are not tax deductible because they are not tax qualified.

- Many hybrid plans do not require a medical exam to get a policy as they use simplified underwriting.